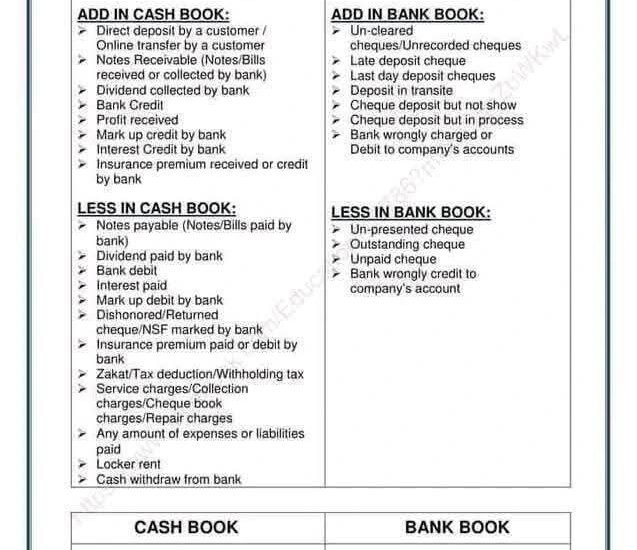

ThIs provides a detailed guide to bank reconciliation, a process used in accounting to ensure that a company’s cash book balance matches the bank statement balance. This is achieved by identifying and adjusting for discrepancies between the two records.

Breakdown and Analysis

The guide is structured into two main sections: adjustments made to the Cash Book and adjustments made to the Bank Book (also known as the Pass Book).

Adjustments to the Cash Book

These adjustments are made for items the company was unaware of until receiving the bank statement:

Additions (Credits by the bank):

Direct deposits/online transfers by customers.

Notes/Bills Receivable collected by the bank.

Dividends, profit, interest, or insurance premiums collected/credited by the bank.

{kind=link}